|

GoGoGadgetChris posted:How much bitcoin should he buy Probably want to weight bitcoin a bit more than lego I mean, your favorite thread is good if I ever need to know which index fund is cheapest by 0.0000001%

|

#

?

Aug 2, 2020 19:32

#

?

Aug 2, 2020 19:32

|

|

|

|

| # ? May 17, 2024 18:38 |

|

|

SIR, my favorite thread is more concerned with horse weddings and funko pop budgets

|

|

#

?

Aug 2, 2020 19:39

|

|

|

Baddog posted:Well, they can have an office on every corner because they are murdering all their clients with those fees. Why? I've got 20+ years to retirement, a 6 month emergency fund, and no debt beyond a mortgage. Now, if he doesn't have an emergency fund, has high interest debt, loans, short term purchases, etc, then yeah, he probably shouldn't put it all in the market immediately. And sure, he can DCA it in if it makes him feel better. You realize people in both threads are pretty much on the same page, right?

|

|

#

?

Aug 2, 2020 19:42

|

|

|

I'm a living example of "don't try to time the market" as around RRSP (Canadian Registered Retirement Plan thingy) contribution time in Jan/Feb I sold some equities and made some contributions, had $40k in cash sitting in it, but then given the um, pandemic, decided to cool my heels a bit instead of doing a normal buy of a few diversified ETFs. Now of course the market exploded and I missed out on gains. So of course I should probably get off the sidelines and do something with this $40k. Do I: 1) do a normal buy of a few diversified ETFs (don't try to time the market u dumbass!!!) 2) Avoid ETF exposure to bad sectors (ie. casinos, cruises, airlines) and put everything in FAANG stocks that are probably less impacted by any looming covid recession? (wait aren't I timing the market again....) 4) other?

|

|

#

?

Aug 2, 2020 20:54

|

|

|

Residency Evil posted:Why? I've got 20+ years to retirement, a 6 month emergency fund, and no debt beyond a mortgage.

|

|

#

?

Aug 2, 2020 20:56

|

|

|

Residency Evil posted:

No not really, I got screeched out of there for saying that someone who showed up with their life savings in cash shouldn't dump it all into the market in the face of the worst health crisis we've had in 100 years. The SP500 hasn't even been around for 100 years. Seems like a similar situation as this guy, except we are six months farther along. If he has nearly all of his money in a savings account, he can afford to ease into the market. And should be aware that he probably still needs a big cash cushion in case things go south from here. Over nearly any time horizon, it isn't going to matter a whole lot if he gets in tomorrow or six months from now - but getting it all in tomorrow will *probably* be a ton riskier. The one size fits all advice is fine for 90%+ of people and situations, but being dogmatic about it and ignoring risk management is pretty dumb for the small percentage of times where it matters.

|

|

#

?

Aug 2, 2020 21:03

|

|

|

If they have an e-fund, a long time until retirement, and no debt beyond a mortgage, what's the risk that needs managing exactly?

|

|

#

?

Aug 2, 2020 21:14

|

|

|

If you are Canadian buy a Nissan Skyline R34 of some kind and sit on it until it's legal in the States to sell to someone there. Canada can import at 15 years and USA is 25 years. You can totally take advantage of that difference. Somehow.

numberoneposter fucked around with this message at 21:23 on Aug 2, 2020 |

|

#

?

Aug 2, 2020 21:21

|

|

|

numberoneposter posted:If you are Canadian buy a Nissan Skyline R34 of some kind and sit on it until it's legal in the States to sell to someone there. Canada can import at 15 years and USA is 25 years. You can totally take advantage of that difference. Somehow. Could be done if I could find some cheap af parking. Would probably have to be way outside of Vancouver as monthly costs for parking here are like minimum $90, and you'd be paying $10k to hold a car for 10 years. That would be pretty fun to do. I knew about Nissan Figaro's and Paos years ago because they are a fairly common site around town, but never came up with the idea to buy and hold before the Americans were able to get their paws on them. I assume they've appreciated in price quite a bit and are more expensive to buy at Japan auction now. But no my money is in a registered account so I can't take it out at this point. Can only buy equities.

|

|

#

?

Aug 2, 2020 21:36

|

|

|

Hoodwinker posted:If they have an e-fund, a long time until retirement, and no debt beyond a mortgage, what's the risk that needs managing exactly? Can't really remember what you said before, but apparently you can't remember what I said either, so we're even. The risk that needs managing is that of needing a lot longer before potential retirement, or retiring with a lot less than they could have. This is a really high risk period of time. Telling someone to YOLO all their savings into an SP500 index asap is a lot loving riskier than it was last year. Can we agree on that at least? Its worked out so far this year, but just because it happened to work out doesn't mean just accepting that increased risk was the smartest thing to do.

|

|

#

?

Aug 2, 2020 21:47

|

|

|

Hoodwinker posted:If they have an e-fund, a long time until retirement, and no debt beyond a mortgage, what's the risk that needs managing exactly? baddog seems concerned with reducing drawdown [1] so that, a year from now, the investor may have more money in his retirement funds than if he otherwise did nothing. [1] https://www.investopedia.com/terms/d/drawdown.asp That type of risk management approach would seek to increase the Sharpe Ratio of the investor: https://www.investopedia.com/terms/s/sharperatio.asp In fact, the long-term thread itself endorses risk management [3], but typically only in the form of suggesting a fixed percentage of bonds in an investment portfolio, such as found in a target date fund, three-fund portfolio, or 60/40 balanced fund. [3] https://www.investopedia.com/terms/r/riskmanagement.asp Risk is everywhere in the market. It's absurd that it is essentially ignored as a concept (by some posters) if someone has a sufficiently long time horizon.

|

|

#

?

Aug 2, 2020 21:48

|

|

|

RE: Garmin - they paid the ransom e: 'allegedly' (lol) BlackMK4 fucked around with this message at 22:00 on Aug 2, 2020 |

|

#

?

Aug 2, 2020 21:56

|

|

|

I love risk. It makes my balance go up over time! Brrrrrr

|

|

#

?

Aug 2, 2020 21:57

|

|

|

Baddog posted:No not really, I got screeched out of there for saying that someone who showed up with their life savings in cash shouldn't dump it all into the market in the face of the worst health crisis we've had in 100 years. The SP500 hasn't even been around for 100 years. As the source of the current thread titles, its absolutely a problem with that thread that some posters refuse to acknowledge that any form of informed choice is possible. E: I also messed up, it should be 'perpetual' not permanent

|

|

#

?

Aug 2, 2020 22:01

|

|

|

Alchenar posted:As the source of the current thread titles, its absolutely a problem with that thread that some posters refuse to acknowledge that any form of informed choice is possible. Not to be argumentative, but what is the problem? And how do you figure there's no informed choice? I'd love to hear more thoughts than just a general musing.

|

|

#

?

Aug 2, 2020 22:02

|

|

|

Anyone throwing in on AAPL assuming the post split means it's going to hit an ATH due to Robinhood and others? Bought $10k in stock at $411ish on Friday

|

|

#

?

Aug 2, 2020 22:13

|

|

|

DoubleT2172 posted:Anyone throwing in on AAPL assuming the post split means it's going to hit an ATH due to Robinhood and others? Bought $10k in stock at $411ish on Friday I intend on picking up 25 or 50 shares before the split. Hopefully not a terrible idea.

|

|

#

?

Aug 2, 2020 22:17

|

|

|

DoubleT2172 posted:Anyone throwing in on AAPL assuming the post split means it's going to hit an ATH due to Robinhood and others? Bought $10k in stock at $411ish on Friday Fractional shares are on Robinhood fyi, not sure if this factors into your bet.

|

|

#

?

Aug 2, 2020 22:30

|

|

|

Baddog posted:Can't really remember what you said before, but apparently you can't remember what I said either, so we're even. 1. They need it a lot longer before potential retirement. 2. They are retiring with a lot less than they could have. Number one needs to be examined from the lens of what events could cause them to need money beforehand. We accept as a group that an e-fund covers a nominal amount of less catastrophic risks - for instance, you lose your job and it takes you several months to find another one. We don't accept an e-fund as sufficient for something like a permanent injury that limits your future earnings significantly. For a risk like this, there is long-term disability insurance. If we enumerate through many of the various forms of catastrophic risk that exist - you get in a serious car accident, a storm rips the roof off of your house, you are temporarily injured and cannot work - we find that a lot of those already have insurance products that cover them. Before we get to the point where we say, "You need to make sure you're managing your investment risk properly in case you need that money sooner," we really need to take a look at whether or not somebody is addressing those risks through existing products - ones which are often better tailored to the financial impact of that risk. I'll admit that the long-term thread generally doesn't have this conversation, but that's I think because the thread focuses primarily on just the investing side of things. Number two needs to be reframed. It's not a problem to retire with less (even a lot less) than you could have as long as you end up having enough to retire and last you until you die. I understand, and there's no argument: having more money overall increases the likelihood that you have enough. But a lot of new investors don't know what "enough" is yet, and I've seen the long-term thread tell a shitload of people to hold off making any serious decisions for weeks/months/a year more than I've ever seen the thread tell somebody to YOLO anything. The issue with telling new investors that it's too risky to do anything now is that it's not calibrating them for a solution as to when it's no longer too risky. Posters from both threads should be very aware how much of this all is the psychological component. The long-term thread focuses on a strategy that gives laypeople a high chance of succeeding in the "good enough" category and allows them arms distance from making too many decisions where psychology starts to kick in. Given a sufficient time frame, the strategy works because it requires minimum psychological involvement: follow the algorithm, wait 30 years, good enough. We do agree: investing into the S&P right now has a higher chance of it becoming less than the same time last year. What I don't agree with is that it is necessarily an inhibiting factor to somebody investing right now for 20-30 years in the future to reach their savings goals. pmchem posted:baddog seems concerned with reducing drawdown [1] so that, a year from now, the investor may have more money in his retirement funds than if he otherwise did nothing. I appreciate your explicit use of definitions here so we're on the same page about terms. I'm not concerned with reducing drawdown, and in general I support a very general strategy for the vast majority of investors that doesn't concern themselves with it either. I expect that over the total course of my investment period, I will experience several drawdowns (possibly even some severe ones), but that the net result will be that I reach my financial goals. I do this because I don't expect to need to concern myself with it. I have this expectation because it's relatively well-supported. I have shored up my financial future in the form of living a modest lifestyle, giving myself a long time frame, and working in a currently high-earning field to ensure that I have additional wiggle room. This is my risk management. I can handle risks to any of these factors (my lifestyle wildly increases suddenly, my time frame gets drastically reduced, or my field/career ends suddenly) in other ways, but I reduce the amount of mitigation that comes from complicating my investment process to a minimum. The reason market risk is largely ignored is that both time horizon and portfolio diversification do seem to manage that risk sufficiently.

|

|

#

?

Aug 2, 2020 22:36

|

|

|

Hoodwinker posted:The long-term thread focuses on a strategy that gives laypeople a high chance of succeeding in the "good enough" category and allows them arms distance from making too many decisions where psychology starts to kick in. Given a sufficient time frame, the strategy works because it requires minimum psychological involvement: follow the algorithm, wait 30 years, good enough. I think the long term thread should be rebranded to "the thread for general strategy which should work if historical trends hold, for people who can't be bothered". That's great, a lot of people need that. Doing god's work, as long as the US maintains its position as the driver of the world economy. (Will it after this? Will it 30 years from now?) But realize that while telling people they should throw the majority of their cash savings into the market asap should eventually work if things keep going like they have been the last 60-70 years - its really goddamn risky right now. And maybe they aren't going to have the stomach for it when the market corrects again. This isn't about "personal risk tolerance" either - the entire world economy is a really loving risky place right now. Hoodwinker posted:We do agree: investing into the S&P right now has a higher chance of it becoming less than the same time last year. What I don't agree with is that it is necessarily an inhibiting factor to somebody investing right now for 20-30 years in the future to reach their savings goals. I think you are conflating risk and expectation of return. You shouldn't accept higher risk without a higher expected return, and you are admitting that you are taking on higher risk (large variance in potential outcomes) along with a lower expectation. Because "it'll probably work out in 20 years, plus I have stocks and bonds".

|

|

#

?

Aug 3, 2020 01:55

|

|

|

and thus we see the proof that index investing may be simple, but that doesn't mean it's easy to understand

|

|

#

?

Aug 3, 2020 02:08

|

|

|

Can you post an actionable alternative strategy? What metric should we be using to sell and buy back in? Buying puts at the right time against one recession once is one thing, buying puts aggressively against 10 of the last 2 recessions gives you much lower returns.

|

|

#

?

Aug 3, 2020 02:11

|

|

|

Hoodwinker posted:I appreciate your explicit use of definitions here so we're on the same page about terms. I'm not concerned with reducing drawdown, and in general I support a very general strategy for the vast majority of investors that doesn't concern themselves with it either. (words about personal goals) I'm not sure that I agree with your risk assessment at all in this environment. See, for example, a discussion of bond convexity here: https://portfoliocharts.com/2019/05/27/high-profits-at-low-rates-the-benefits-of-bond-convexity In particular, long T-Bonds are historically used as a popular hedge for stocks, and the quote from above is quite relevant today: "Low-interest 30-year bonds are very volatile! In fact, the range of returns is similar to what you might expect from the stock market." Total bond index funds, of course, are more boring than long T-Bonds. You mention diversification, but also that you're not concerned with reducing drawdown -- I mean, the point of diversification with bonds as used in most target date or similar balanced funds is specifically to reduce drawdown. I use those as examples because those are the generally accepted conventional wisdom set-and-forget long-term investing approaches. But if you want "diversification" "to manage that risk", then, if you're also an investor who CAN be bothered to deal with their investments, does it really make sense to limit yourself to both: (a) a fixed strategy regardless of macro circumstances, such as a 60/40 fund or boglehead 3-fund, and (b) only using bonds as a diversification tool, instead of a whole arsenal of financial options including allocations to cash, gold, inflation-protected securities, or options? I'd argue that the answer to both should be "no". For example, in question (a), an investor may have a certain risk tolerance. For the typical year, let's say a "60/40 balanced fund" fits that person's risk tolerance. That's a fairly risk averse investor. Then let's say a nuclear war happens, shutting down worldwide trade and closing down economies, crippling megacities. Or maybe just a pandemic that does the same thing. Clearly, RISK has gone up. That investor, if trying to be as greedy as possible within their risk tolerance, should probably adjust their asset allocation to be more conservative. As for (b), I think that's much more accepted by most serious individual investors. But it takes effort, options are complicated, some people don't believe it gold, etc. It's not for everyone. It's certainly not for the long-term thread. But it fits in this thread. See, for example, this risk parity ETF as an investment option which combines major asset types: https://rparetf.com/rpar Frankly, I'm 100% in stocks right now not because I don't think they're risky, but because I think long T-Bonds are an even worse play at the moment. I kind of wish I had reallocated some into gold a few weeks ago, but, I did not expect it to outperform T-Bonds like it has lately (check out this relation to real yields: https://themarketear.com/posts/cZdJnJTapE ; lots of discussion on that front lately on twitter). I might find an alternative commodity play or just go cash if Congress can't get its poo poo together soon. Put options make sense too. Heck, maybe just go RPAR for a bit. But if Congress and the Fed keep that money flowing, then my equity ETFs should win out over all time horizons.

|

|

#

?

Aug 3, 2020 03:01

|

|

|

Baddog posted:I think the long term thread should be rebranded to "the thread for general strategy which should work if historical trends hold, for people who can't be bothered". That's great, a lot of people need that. Doing god's work, as long as the US maintains its position as the driver of the world economy. (Will it after this? Will it 30 years from now?) But realize that while telling people they should throw the majority of their cash savings into the market asap should eventually work if things keep going like they have been the last 60-70 years - its really goddamn risky right now. And maybe they aren't going to have the stomach for it when the market corrects again. This isn't about "personal risk tolerance" either - the entire world economy is a really loving risky place right now. I think you're conflating your perception of risk with actual risk. We agree that it seems likely that the S&P is going to be pretty volatile in the next year. Except, the market doesn't give a poo poo what we think. The government is literally pumping trillions of dollars into the market right now. I'm not going to pretend that my perception of market risk is accurate. Why do you think yours is? Hoodwinker fucked around with this message at 03:25 on Aug 3, 2020 |

|

#

?

Aug 3, 2020 03:10

|

|

|

pmchem posted:It's certainly not for the long-term thread. But it fits in this thread. See, for example, this risk parity ETF as an investment option which combines major asset types: https://rparetf.com/rpar I will speak to your rebuttal of my comment about "not reducing drawdown" that I did a poor job of stating my position: I'm not concerned with reducing dramatic drawdown by hedging risk during major downturns via things like options or gold or cash. I understand the place of bonds in reducing volatility in a portfolio. Mine has 10% bonds in it for this reason (and to give me something to rebalance with).

|

|

#

?

Aug 3, 2020 03:17

|

|

|

Edit wrong thread.

|

|

#

?

Aug 3, 2020 03:23

|

|

|

crazypeltast52 posted:Can you post an actionable alternative strategy? Obviously there isn't any silver bullet. This is the first time in my 25 years of investing that I bought protective puts. In 2007, I sold my house and went back to renting because everyone who was paying attention knew the real estate market was hosed - but I didn't take that next step to figure out what else I should be doing. In no way am I saying taking action at the right time is easy - but after 2001 I did learn to try to cover my rear end if I think a train is coming. I'd love to talk about strategies for diversification beyond stocks and bonds. I've gotten into all kinds of poo poo. The "one strategy to rule them" thread thought it was hilarious to have property and currency in another country, but now I wish we had more than one bolthole (any recommendations?). A bunch of my "cash" is in tips now. I do have metal funds. I've got a chunk in predictit picking up pennies, but it's harder to get returns as your roll grows (although I'm still doing 10% a year). Yes, I bought bitcoins way back when. I did that peer to peer lending site (sucked). I'd like to hear about anything.

|

|

#

?

Aug 3, 2020 04:08

|

|

|

alright frienjds i need to make about $2,600 this week off of my $600 in Robinhood to keep my house. which calls am i doing

|

|

#

?

Aug 3, 2020 10:39

|

|

|

err posted:alright frienjds i need to make about $2,600 this week off of my $600 in Robinhood to keep my house. Suicide hotline?

|

|

#

?

Aug 3, 2020 11:26

|

|

|

leper khan posted:Suicide hotline? That�s next week

|

|

#

?

Aug 3, 2020 12:01

|

|

|

leper khan posted:Suicide hotline?

|

|

#

?

Aug 3, 2020 13:46

|

|

|

I have like 100 shares of GOOGL from last week but also got shares in AAPL, NVDA, MSFT all bought during the small mega cap tech dip. Haven't taken profits on AMD but I might just take it since the stock is stalling or put a profit taker nearby. Got out of PINS completely post earning and rerolled half of the profit into calls for this week, already up 200%, I have completely reduced my options trading and it has increased my monthly returns so much. I am totally fining holding stocks through volatility but I sold itm aapl calls for end of august in -50% loss and bought stock instead of it. Would have made probably double what I am in profit now.

|

|

#

?

Aug 3, 2020 14:58

|

|

|

Baddog posted:No not really, I got screeched out of there for saying that someone who showed up with their life savings in cash shouldn't dump it all into the market in the face of the worst health crisis we've had in 100 years. The SP500 hasn't even been around for 100 years. Take a look at this: https://towardsdatascience.com/monte-carlo-simulation-with-dollar-cost-averaging-653ae47ec7d5 You're right. DCA is less "risky" than investing a lump sump, but on average, you're going to get a higher investment return over the long run by investing a lump sum immediately. We lost what felt like a lot of money between all of our accounts in March/April. I kept on investing mindlessly every month. Now I'm back up. You know why I didn't lose much sleep? I had cash in an emergency fund, knew that my investments would eventually come back, and wasn't worried about what trades I was going to make in my accounts. My portfolio is 90% equities, 10% bonds (not including cash). Aggressive, but the market downturn didn't make me nervous, which was helpful in teaching me that I'm ok with the risk in my asset allocation.

|

|

#

?

Aug 3, 2020 15:18

|

|

|

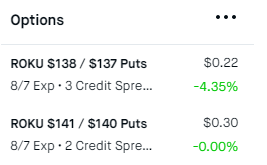

err posted:alright frienjds i need to make about $2,600 this week off of my $600 in Robinhood to keep my house. The one to the personal loan banker But that said, I'm big into ROKU because none of my other orders were filled this moring, and ATVI looks pretty good right now

|

|

#

?

Aug 3, 2020 15:44

|

|

|

Ok fk just closed half of my position on AMD, the profits were too good not to take. I sold AMD early once at $35 but this is a pretty volatile stock and whenever it loses momentum it can pull back nastily. My cost basis $40 so I don't mind any immediate pullback, will have time react to a sell off to put a stop in . AMD, SVXY and precious metals were my largest position post covid-19 crash . So all those worked wonderfully. SLV i made a massive mistake of not using stop loss and just selling it myself but I learned a lesson from that. Put positions on GOOGL and FDX. I might also get ATVI just for earning. I had ea which I sold post earning. I don't like buying options into earnings so I just might get 100-200shares with tight stop loss. I do think their earnings should be good but how much of the free CoD is priced in or how well did perform. I do think it will be a beat on estimates but not sure by how much. Ulio fucked around with this message at 16:06 on Aug 3, 2020 |

|

#

?

Aug 3, 2020 16:00

|

|

|

Anyone else still nudging more into $SOLY? Also I touched ATVI poop.

|

|

#

?

Aug 3, 2020 16:34

|

|

|

ATVI is going to benefit massively from people sitting at home buying lootboxes so that poop is about to look like this I would have got some too but my entire account is tied up in ROKU and AMD right now.

|

|

#

?

Aug 3, 2020 16:45

|

|

|

movax posted:Anyone else still nudging more into $SOLY? I would think SOLY wouldn't be doing too hot short term since similar to tattoos people can't really use it's services right now safely (they make the tattoo removal machine or whatever right?).

|

|

#

?

Aug 3, 2020 16:54

|

|

|

tangy yet delightful posted:I would think SOLY wouldn't be doing too hot short term since similar to tattoos people can't really use it's services right now safely (they make the tattoo removal machine or whatever right?). Yeah, tattoo removal. It just had a massive erasure of market cap / stock price drop after offering up some crazy amount of shares again.

|

|

#

?

Aug 3, 2020 17:41

|

|

|

|

| # ? May 17, 2024 18:38 |

|

|

This on ATVI is basically a free 12% return on your capital. There's basically no way ATVI drops this low, if it drops at all, it would have to lose 15% of its market cap after earnings during a time where video game companies that have micro transactions are smashing every quarter: edit: Plus the earnings IV crush would work in your favor here anyways so even if it does go down, you'll probably end up winning regardless AHH F/UGH fucked around with this message at 18:00 on Aug 3, 2020 |

|

#

?

Aug 3, 2020 17:54

|

|