|

silicone thrills posted:Answer to the above - It specifically says 25% of base pay. It isn't the match i'm talking about. That seems like it should be illegal, but I don't even know how to find out for sure.

|

#

?

Mar 15, 2017 16:11

#

?

Mar 15, 2017 16:11

|

|

|

|

| # ? May 23, 2024 15:27 |

|

|

silicone thrills posted:I'm the low earner in my relationship if that helps put it into perspective. I'm 29 and we have the potential to be FI in about 6-7 years if we keep on track. Weirdest one I've seen is accounting software that only lets me contribute an integer percentage of my paycheck to a retirement account. This meant I couldn't max it out, because n% was under the annual limit but (n+1)% was over it. The benefits guy who was configuring it for me seemed very confused and mystified by me wanting anything else so I dropped it.

|

|

#

?

Mar 15, 2017 16:17

|

|

|

So I had a really nauseating moment in macroeconomics the other week where the professor - really charming guy - goes off on a tirade about the end of growth and pointed toward our demographic boom coming of age during a severe financial downturn as evidence that the long honeymoon would be over - that all of this stuff, large-scale trends away from consumption and toward frugality, spending less, financial independence - would come back to bite us by destroying the engine that brought us to this point.

|

|

#

?

Mar 15, 2017 16:18

|

|

|

EAT FASTER!!!!!! posted:So I had a really nauseating moment in macroeconomics the other week where the professor - really charming guy - goes off on a tirade about the end of growth and pointed toward our demographic boom coming of age during a severe financial downturn as evidence that the long honeymoon would be over - that all of this stuff, large-scale trends away from consumption and toward frugality, spending less, financial independence - would come back to bite us by destroying the engine that brought us to this point. Everyone has their personal reasons for frugality and mine are a direct consequence of the inability to take financial risks in our social structure because we could literally end up starving to death on the street. Bhodi fucked around with this message at 16:25 on Mar 15, 2017 |

|

#

?

Mar 15, 2017 16:22

|

|

|

silicone thrills posted:Answer to the above - It specifically says 25% of base pay. It isn't the match i'm talking about. I have seen online software that caps out at 25% - I never pushed it because 25% was enough to max, but I always kind of wondered if someone in HR could override that. Companies that don't offer a 3% safe harbor contribution are also subject to highly compensated employee rules, where a highly salaried (>120k or so?) employee is limited to a low contribution based on a bunch of factors. I think 25% is also the contribution limit for some IRA based retirement profit sharing plans like a SEP and SIMPLE IRA, so maybe they have some weird overlap or structure involving one of those instead of a true 401k.

|

|

#

?

Mar 15, 2017 16:26

|

|

|

Jeffrey of YOSPOS posted:Weirdest one I've seen is accounting software that only lets me contribute an integer percentage of my paycheck to a retirement account. This meant I couldn't max it out, because n% was under the annual limit but (n+1)% was over it. The benefits guy who was configuring it for me seemed very confused and mystified by me wanting anything else so I dropped it. Every 401(k) I've seen won't let you overcontribute. If the percentage you choose results in overcontribution you'll simply not get as much taken out of your last paycheck(s). My current Fidelity 401(k) is like this, and even has a separate contribution percentage for roth.

|

|

#

?

Mar 15, 2017 16:43

|

|

|

Bhodi posted:Everyone has their personal reasons for frugality and mine are a direct consequence of the inability to take financial risks in our social structure because we could literally end up starving to death on the street. But capitalism rewards hard work!!!

|

|

#

?

Mar 15, 2017 16:44

|

|

|

Jeffrey of YOSPOS posted:Weirdest one I've seen is accounting software that only lets me contribute an integer percentage of my paycheck to a retirement account. This meant I couldn't max it out, because n% was under the annual limit but (n+1)% was over it. The benefits guy who was configuring it for me seemed very confused and mystified by me wanting anything else so I dropped it.

|

|

#

?

Mar 15, 2017 16:52

|

|

|

Motronic posted:Every 401(k) I've seen won't let you overcontribute. If the percentage you choose results in overcontribution you'll simply not get as much taken out of your last paycheck(s). Simple IRA does not have a percentage maximum for you, though it does have a maximum employer match of 3% of your salary.

|

|

#

?

Mar 15, 2017 16:52

|

|

|

Bhodi posted:I want to punch the idea into him that when we stopped investing in the future by subsidizing education and removing social safety nets and enacted programs that concentrated wealth upward that's what has actually destroyed the engine We're approaching year 10 of a bull market so I think it's premature to complain about a broken engine. Even if it is broken I think it's hard to blame education funding since more people have college degrees than ever. And the US has seen strong economic growth compared to many countries that subsidize education more than we do, France for example. I think if returns start slowing it's because we don't have the next big invention to drive productivity growth yet. The industrial revolution kicked off in the 1800s and we got steam power, oil, chemicals, pharmaceuticals, cars, airplanes, nuclear and all sorts of totally new stuff that completely changed the world and gave us a ton of growth. Then the 1960s-1970s hit and we had computers which were almost as big of a deal. Now we have computers that are so fast that making them slightly faster doesn't help as much, we only get small incremental improvements. Going from having no computer to a slow computer makes me a much more productive engineer. Going from a slow computer to a fast computer makes me slightly more productive. Going from a fast computer to a really fast computer only helps a tiny bit. So rapid, sustained growth like we saw before is going to be difficult until somebody comes out with the next big thing.

|

|

#

?

Mar 16, 2017 04:21

|

|

|

Super Dan posted:That seems like it should be illegal, but I don't even know how to find out for sure. I work for one of the biggest companies in the US, and we have a 30% contribution limit as well. I asked HR if I could go over and was told no.

|

|

#

?

Mar 16, 2017 04:34

|

|

|

OctaviusBeaver posted:We're approaching year 10 of a bull market so I think it's premature to complain about a broken engine. Even if it is broken I think it's hard to blame education funding since more people have college degrees than ever. And the US has seen strong economic growth compared to many countries that subsidize education more than we do, France for example. I think it's safe to say that equity returns are pretty decoupled from the average American's financial situation. Your parents' DB plans + home equity are likely worth more than a millennial maxing out his 401K. With mass automation looming, something has got to give with wealth distribution in the US.

|

|

#

?

Mar 16, 2017 08:32

|

|

|

OctaviusBeaver posted:We're approaching year 10 of a bull market so I think it's premature to complain about a broken engine. Even if it is broken I think it's hard to blame education funding since more people have college degrees than ever. And the US has seen strong economic growth compared to many countries that subsidize education more than we do, France for example. I feel like the "next big thing" is robotics and AI. I am hoping they alone will be enough to drive economic growth for decades. Self driving cars will change the world. I am very optimistic about economic growth.

|

|

#

?

Mar 16, 2017 10:11

|

|

|

OctaviusBeaver posted:I think if returns start slowing it's because we don't have the next big invention to drive productivity growth yet. The industrial revolution kicked off in the 1800s and we got steam power, oil, chemicals, pharmaceuticals, cars, airplanes, nuclear and all sorts of totally new stuff that completely changed the world and gave us a ton of growth. Then the 1960s-1970s hit and we had computers which were almost as big of a deal. Now we have computers that are so fast that making them slightly faster doesn't help as much, we only get small incremental improvements. Going from having no computer to a slow computer makes me a much more productive engineer. Going from a slow computer to a fast computer makes me slightly more productive. Going from a fast computer to a really fast computer only helps a tiny bit. So rapid, sustained growth like we saw before is going to be difficult until somebody comes out with the next big thing. Robots. If by 'rapid, sustained growth', you mean 'rapid, sustained rise in profits/inequality'.. then the answer is robots. It's already happening. In terms of quality of life improvement, what could be better than a robot doing your job so you don't have to? (Please ignore the fact you are now unemployed) Chadzok fucked around with this message at 02:26 on Mar 17, 2017 |

|

#

?

Mar 17, 2017 02:24

|

|

|

Chadzok posted:Robots. If by 'rapid, sustained growth', you mean 'rapid, sustained rise in profits/inequality'.. then the answer is robots. It's already happening. The way I see it, those of us who are amassing capital for the purposes of freedom can't lose in this scenario. Either we continue along the current path and continue to use the robit's profits to heavily reward those who have capital, or we switch gears and more evenly distribute the robit's profits. In the latter case this still benefits those of us who are in the FI game for freedom, because it means the cost of living should go down, allowing us to draw down less of our portfolios each year.

|

|

#

?

Mar 17, 2017 14:12

|

|

|

if you have more than a year's salary in investments you're already so far ahead of the curve in the usa that the "average american" in virtually any scenario may as well not apply to you.

|

|

#

?

Mar 18, 2017 14:12

|

|

|

Bhodi posted:if you have more than a year's salary in investments you're already so far ahead of the curve in the usa that the "average american" in virtually any scenario may as well not apply to you. This is unfortunately the case. If you have a house and a year's worth of pay invested then you are even further ahead. It seems that New Zealand has the same retirement saving problem as the US. People keep tapping into their retirement savings for financial emergencies (that seem to occur on a very regular basis).

|

|

#

?

Mar 20, 2017 04:11

|

|

|

If only there were some way to know I was going to want a brand new truck 2 years after I got my last brand new truck. Better liquidate my account before those banksters drain it all away with their Ponzis and credit swap tricks and GET WHAT I'M OWED!

|

|

#

?

Mar 20, 2017 04:18

|

|

|

In New Zealand there is a requirement to demonstrate that there is a financial emergency. However having bills to pay and no money seems to be sufficient to tap into it. Seems easy enough to manufacture an emergency. Although I have friends who would like to be able to tap into it partially to reduce the size of their mortgage and the monthly payments to create some breathing room in their budget. However, that isn't an emergency.

|

|

#

?

Mar 20, 2017 04:24

|

|

|

Devian666 posted:In New Zealand there is a requirement to demonstrate that there is a financial emergency. However having bills to pay and no money seems to be sufficient to tap into it. Seems easy enough to manufacture an emergency. What kind of hand-holding country are you living in? Is there a penalty for withdrawal? Here in Canada you can tap into your RRSP for heroin if you want to, but you give up the contribution room forever and you have to pay tax on it (since you didn't pay tax on it when you contributed). Again, they don't care what it's for. Unless it's for a house as a first-time home buyer, or education; then there's no penalty as long as you pay it back over X years. Basically, since most people see the money as being locked-in when you put it into an RRSP, most people just don't contribute, lol. Which is probably worse than what you're talking about. Rick Rickshaw fucked around with this message at 12:26 on Mar 20, 2017 |

|

#

?

Mar 20, 2017 12:17

|

|

|

Bhodi posted:if you have more than a year's salary in investments you're already so far ahead of the curve in the usa that the "average american" in virtually any scenario may as well not apply to you. Sometimes it doesn't feel that way. I've got enough income to max out my tax advantaged accounts leaving me with enough to live a slightly better lifestyle than some of my less well off neighbors. Since real estate is expensive compared to income here I live in a 2 bed 1.5 bath condo while public assistance housing has rent subsidized 2 bed 1 bath places of similar size. It will be years and years and years until I think I can afford a 4 bedroom 2.5 bath 2 car garage style house my parents have. I make maybe 3 times the household income compared to low income people and the most visible thing I get out of it is an extra toilet and sink. Why am I not buying an outsized truck like some of my neighbors or an outsized mortgage instead of saving for this retirement thing that could be decades away?

|

|

#

?

Mar 20, 2017 20:23

|

|

|

Crazy Mike posted:Sometimes it doesn't feel that way. I've got enough income to max out my tax advantaged accounts leaving me with enough to live a slightly better lifestyle than some of my less well off neighbors. Since real estate is expensive compared to income here I live in a 2 bed 1.5 bath condo while public assistance housing has rent subsidized 2 bed 1 bath places of similar size. It will be years and years and years until I think I can afford a 4 bedroom 2.5 bath 2 car garage style house my parents have. Bhodi fucked around with this message at 21:00 on Mar 20, 2017 |

|

#

?

Mar 20, 2017 20:56

|

|

|

Bhodi posted:Statistically speaking, you probably won't ever reach the prosperity and wealth of your parents if you're under 35. Especially not in real estate. But never fear, the hedonic treadmill ensures that except for a little burst of pleasure at the front end you won't be any happier owning any of it anyway, and compared to your neighbors you'll get to retire earlier and in significantly more comfort than them. You're also in a much better position to weather downturns in life like injury or illness. I really love this article but again - ding ding ding - it raises the alarm at the arrest of growth.

|

|

#

?

Mar 20, 2017 21:05

|

|

|

Rick Rickshaw posted:What kind of hand-holding country are you living in? Is there a penalty for withdrawal? As usual it's an issue of local politics. The Government is entirely focused on baby boomers and they don't care what happens to the younger generations. The withdrawals are allowed but something to keep in mind is most of the money going in is post-tax dollars. There's only a small tax credit of $521 per year (which is obviously crap). There's no penalty or required repayments leaving the only penalty of being hosed when they reach retirement age. There are also the first home buyer exceptions and benefits that mostly don't work because of over inflated house prices. People contribute as it's often a part of a negotiated package with their employer but the contributions are 3% employee and 2-3% employer in most cases. For most of the population that's not going to add up to much of a retirement and most low wage earners are in the wrong tax code for their retirement account.

|

|

#

?

Mar 20, 2017 22:11

|

|

|

Bhodi posted:But never fear, the hedonic treadmill ensures that except for a little burst of pleasure at the front end you won't be any happier owning any of it anyway.

|

|

#

?

Mar 21, 2017 01:41

|

|

|

That's a fairly flawed study, fake fichmech. It's chief source of data is self-reporting gallup polls and in closing paragraphs it even acknowledges that it's at odds with the prevailing theory and that there was an interesting study done which presented opposing results. I also liked this footnote: "While 100 percent of those reporting annual incomes over $500,000 are in the top bucket of �very happy,� it is important to note that there are only eight individuals in this category". Bhodi fucked around with this message at 02:10 on Mar 21, 2017 |

|

#

?

Mar 21, 2017 02:06

|

|

|

Bhodi posted:That's a fairly flawed study, fake fichmech. It's chief source of data is self-reporting gallup polls and in closing paragraphs it even acknowledges that it's at odds with the prevailing theory and that there was an interesting study done which presented opposing results. quote:We are intrigued by these findings, although we conclude by noting that they are based on very different measures of well-being, and so they are not necessarily in tension with our results. Indeed, those authors also find no satiation point for evaluative measures of well-being

|

|

#

?

Mar 21, 2017 02:10

|

|

|

Ralith posted:The "more money won't make you happier" meme is probably nonsense. I really enjoy Table 2 of this study. Does it maybe have statistical shortcomings? Sure, whatever, but on the other hand the idea that money isn't a significant source of stress beyond 75k or whatever stupid number gets bandied about is preposterous. I have to tell you, I feel a lot happier in the lower bucket than the higher one.

|

|

#

?

Mar 21, 2017 13:42

|

|

|

EAT FASTER!!!!!! posted:I really enjoy Table 2 of this study. Does it maybe have statistical shortcomings? Sure, whatever, but on the other hand the idea that money isn't a significant source of stress beyond 75k or whatever stupid number gets bandied about is preposterous. I have to tell you, I feel a lot happier in the lower bucket than the higher one. I bet that it's less about income in absolute terms and more about overhead; how consistently can you keep your expenses within your income with what kind of variance? Having been laid off twice, it was way less stressful with over a year of expenses socked away and readily liquid than it was with about a month left in my checking account. It's easier to get to that point with more income if you are mature and responsible with it. I'd be really curious to see the results if you measured for income & also just correlated on self-reported budgeting + meeting that budget on some consistency.

|

|

#

?

Mar 21, 2017 15:05

|

|

|

That looks like another one of those studies that doesn't differentiate income and wealth. 250k probably doesn't make you too much happier if you burn through your paychecks each month, but there's a pretty good chance you're happy if you make 30k working at a vet's office with a few million in the bank.

|

|

#

?

Mar 21, 2017 15:25

|

|

|

Outside of the 1%ers, income is probably pretty highly correlated with wealth.

|

|

#

?

Mar 21, 2017 16:44

|

|

|

shrike82 posted:Outside of the 1%ers, income is probably pretty highly correlated with wealth. I'm not so sure about the correlation for people with postive wealth though - a 10 year moving average of income or something like that might work better but I don't know. We are specifically talking about whether or not the "money stops buying happiness at 75k" urban legend is true though, which requires talking about generally high-income earners. I think that group is pretty likely to have a disparity between wealth and income. Jeffrey of YOSPOS fucked around with this message at 17:01 on Mar 21, 2017 |

|

#

?

Mar 21, 2017 16:52

|

|

|

Sorry, I just found the two scenarios you set up kinda funny - 250K household or a millionaire making 30K. Maybe the latter's more common than I think but it comes off as implausible.

|

|

#

?

Mar 21, 2017 17:08

|

|

|

shrike82 posted:Sorry, I just found the two scenarios you set up kinda funny - 250K household or a millionaire making 30K.

|

|

#

?

Mar 21, 2017 17:10

|

|

|

If nothing else, housing should cause those who make more to gain more wealth.

|

|

#

?

Mar 21, 2017 17:15

|

|

|

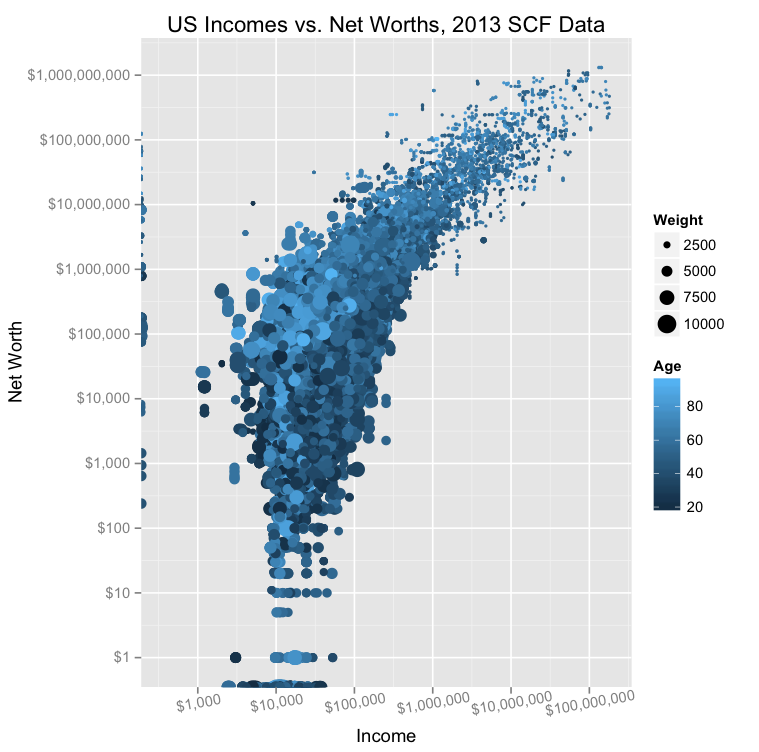

C'mon, there's no need to pull numbers out of your rear end:

|

|

#

?

Mar 21, 2017 17:29

|

|

|

also stop using papers about gdp vs happiness at a national level in a discussion about individual gdp vs happiness

|

|

#

?

Mar 21, 2017 17:36

|

|

|

shrike82 posted:Sorry, I just found the two scenarios you set up kinda funny - 250K household or a millionaire making 30K. I'd say it's pretty common...for people whose parents were/are millionaires.

|

|

#

?

Mar 21, 2017 17:36

|

|

|

Another day, another long-format think piece from an intellectual giant highlighting the problem with the dwindling adult male labor force participation rate and its connection with the death of growth. I don't know that financial independence is attainable without really pumping that "r" - it's in every formula we bank on - and I don't know that you can say r will be > inflation the way the emergence from this last recession has gone.

|

|

#

?

Mar 21, 2017 18:31

|

|

|

|

| # ? May 23, 2024 15:27 |

|

|

coffeetable posted:C'mon, there's no need to pull numbers out of your rear end: Thanks for posting this. It is interesting and shows a fairly clear correlation but it also seems to confirm that there is a big chunk of people with high incomes with comparatively small net worths (wealth). While ~100k income looks to be the start of the inflection point, there's still a whole lot of people in that 100k-250k territory with net worths less than 1 year of their income. Age may play a part of it (younger people haven't had as many years to save as older people), but I don't think that tells the whole story.

|

|

#

?

Mar 21, 2017 18:40

|

|